While there is no fixed formula to create an investment portfolio especially when the risk nature and investment preference of one investor differs from the other, I intend to share my own investment portfolio as a reference for readers.

In creating this investment portfolio, I must highlight the following points:

- This portfolio is created for "lump sum" investing.

- This portfolio is designed for long term investing (more then 5 years)

- This portfolio utilizes the concept of diversification as a strategy to mitigate potential losses of certain investments.

- This portfolio only utilizes unit trust funds due to the huge variety of sectors and geographical investment opportunities available through unit trust investment.

- Another reason for utilizing unit trust fund as a medium of investment is to allow investors to invest passively, This eliminates the need for analyzing and constantly monitoring our investment.

- Before investing into this portfolio, an investor should have additional liquidity/savings not included as part of the investment amount of this portfolio. This liquid savings should be parked into safe zones such as Fixed Deposit Accounts, Lembaga Tabung Haji or even Amanah Saham funds. Liquid savings should be easily withdrawn for emergency use. Recommended liquidity savings is approximately 6 months of your salary.

Creating a Unit Trust Investment Portfolio

The key factors to consider before starting an investment portfolio are:

1. The risk tolerance of the investor

2. The age of the investor and the amount of time available to achieve your investment goal

Knowing your Risk Tolerance

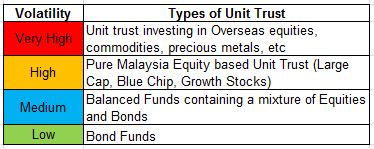

Investing via unit trust carries a certain amount of risk which I term as volatility risk. Volatility risk is the potential fluctuation of profit or loss from the unit trust price you invested in. For example, if you have invested into Unit Trust Fund A at RM1.00 per unit, the movement of unit price above RM1.00 or below RM1.00 is called volatility. The higher the volatility, the bigger the price movement (upward or downward) of a unit trust fund, thereby creating larger profits or vice versa

Principally, volatility risk in unit trust can be categorized into 4 types:

- Very High Volatility (potential gain/loss of 30% or more*)

- High Volatility (potential gain/loss of 15% or more*)

- Medium Volatility (potential gain/loss of 8% or more*)

- Low Volatility (potential gain/loss of 3% or more*)

*Do take note that the potential gain/loss listed above are derived from general observation of the performance of unit trust funds under respective volatility risk group.

From the different kinds of volatility risk listed above, we can now categorized the different types of unit trust according to the table below:

By understanding the risk above, you should be wary that despite the large earning potential of high or very high risk funds, the possibility to lose that amount does exist as well.

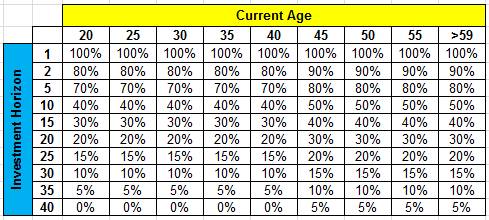

Age of Investor and Investment Horizon

Risk aside, the age of an investors plays an important role when it comes to constructing an unit trust investment portfolio. Generally the younger you are, the more risk you can assume when it comes to investing. After which, the age of an investor must then go hand in hand with the investment horizon of the investor.

For example, a 20 year old investor with an investment horizon of only 3 years cannot take up as much risk as an 30 year old investor with an investment horizon of 10 years.

The reasoning simply boils down to Volatility.

For a 20 year old investor who needs to use his /her investment money within 3 years, capital preservation is vital. "Very high" and "High" volatility unit trust funds should be avoided altogether by this investor in order to eliminate the possibility of suffering losses when the time comes for him/her to withdraw the investment.

In comparison to the 30 year old investor with a 10 year investment horizon, his/her portfolio allocation can be designed to encompass a bigger percentage of "Very High" and "High" volatility of unit trust funds.

What are the Right Percentages for my Unit Trust Investment Portfolio?

Start with allocating a portion of your portfolio to Low or Medium Risk Unit Trust Fund

Remember the "Age of Investor" and "Investment Horizon" I talked about earlier?

Well start by determining your age (duh...) and how long is your investment horizon. Once you have your age and number of years to invest, you can then compare it with the table below:

|

| Table for Low or Medium Risk Unit Trust Fund |

The table above determines how much you should first set aside for investment into a low or medium volatility unit trust funds. If you feel uncomfortable setting that amount to a low risk unit trust fund such as Bond Funds or a medium risk Balanced Fund, you can also allocate that sum of investment to a Fixed Deposit Account, ASB, or even SSPN to enjoy income tax relief, etc.

Diversify your remaining investments to other Unit Trusts

Once you've set aside the allocation for low or medium volatility funds, the remaining of your investment can now be allocated to other unit trust funds.

A simple guideline is to ensure that you have a mix of different kinds of unit trust funds. Search for funds that vary in terms of sectors, nature of investment as well as geographical location. The objective is to select a mixed variety of funds which are not dependent upon each other.

Here's an example of a portfolio made up of 11 different unit trust categories:

Category

|

Justifications

/ Remarks

|

|

World

Equity

|

Search for funds that invest into

stocks of international brands. (Coca Cola, Samsung, Gillette, etc)

Despite any economic downtown, consumer products which are well known around the world will still be consumed. |

|

US

Equity

|

Despite the concern by many about

uncontrolled printing of loose money, the US economy is in fact still at the

recovery stage. Search for funds that invest or tracks the S&P500 for

this category.

|

|

Europe

Inc UK

|

An alternative of investment into

European equities as a form of diversification.

|

|

Asia

Pac Excluding Japan

|

The Asia Pacific market (Hong

Kong, Taiwan, Korea and also Asian Countries have benefited both from China's

growth as well as from domestic demands.

|

|

Asia

Pac Exc Japan (Small & Mid Cap)

|

Captilizing on High Risk Small

& Mid Cap Equities of Asia Pacific countries.

|

|

Asian

Market

|

There's still room for growth

amongst Asian countries which include Malaysia, Thailand and Singapore.

Despite the political unrest in Thailand which have dragged the stock market

down should rebound once the election is over.

|

|

China

|

China is set to benefit for the

next few years once the policies for stable economic growth is put into place

and enforced by the ruling government.

|

|

Malaysia

Equity

|

There's no place like home.

Experienced fund managers have continously outperformed the KLCI by

practicing prudent stock picking.

|

|

Malaysia

Small & Mid Cap

|

Top performing Malaysia Small

& Mid Cap funds have achieved about 30% annual returns in 2013. Despite

the high risk, having some of your investment in category is certainly

worthwhile.

|

|

Gold

& Precious Metals

|

When the stock market crashes,

gold and precious metals set to benefit as investors switch to gold for

hedging purposes. With the recent drop in gold prices, perhaps it wise to

allocate a portion of your portfolio into funds which invest into gold.

|

|

Global

REITS

|

Diversifying into funds that

invest into REITS promotes stability in terms of returns. REITS funds are

also known to be more resilient towards economic downturns

|

|

Do take note that the proposed portfolio serves only as a recommendation. Investor can choose to add or remove categories from this portfolio as he or she see fit.

What Percentage (%) of my portfolio should I allocate for each Category?

Once again the % allocation of the portfolio is based on my personal recommendation. The percentage for each category may change as I tend to review the portfolio every 6 months.

Shown below is the proposed percentage (%) for portfolio allocation:

Category

|

%

Allocation

|

|

Bond

Fund or Balanced Fund

|

X

|

|

World

Equity

|

6.00%

of Y

|

|

US

Equity

|

6.00%

of Y

|

|

Europe

Inc UK

|

5.50%

of Y

|

|

Asia

Pac Excluding Japan

|

7.50%

of Y

|

|

Asia

Pac Exc Japan (Small & Mid Cap)

|

10.00%

of Y

|

|

Asian

Market

|

7.50%

of Y

|

|

China

|

12.00%

of Y

|

|

Malaysia

Equity

|

20.00%

of Y

|

|

Malaysia

Small & Mid Cap

|

8.00%

of Y

|

|

Gold

& Precious Metals

|

10.00%

of Y

|

|

Global

REITS

|

7.50%

of Y

|

|

What is X and Y?

X = Value calculated using % from "Table for Low or Medium Risk Unit Trust Fund"

Y = Remaining investment amount to be allocated according to the percentages of each Category

Example:

- Investor A has RM100,000 to invest. He intends to create a unit trust investment portfolio.

- By looking at the "Table for Low or Medium Risk Unit Trust Fund", Investor A is required to allocate 20% of his investment to Low or Medium Risk Unit Trust Fund.

X = 20% of RM100,000

= RM20,000

Y = RM100,000 - X

= RM100,000 - RM20,000

= RM80,000

Unit Trust Portfolio for Investor A would look something like this:

Category

|

%

Allocation

|

Allocation

(RM)

|

|

Bond

Fund or Balanced Fund

|

X

|

20,000.00

|

|

World

Equity

|

6.00%

of Y

|

4,800.00

|

|

US

Equity

|

6.00%

of Y

|

4,800.00

|

|

Europe

Inc UK

|

5.50%

of Y

|

4,400.00

|

|

Asia

Pac Excluding Japan

|

7.50%

of Y

|

6,000.00

|

|

Asia

Pac Exc Japan (Small & Mid Cap)

|

10.00%

of Y

|

8,000.00

|

|

Asian

Market

|

7.50%

of Y

|

6,000.00

|

|

China

|

12.00%

of Y

|

9,600.00

|

|

Malaysia

Equity

|

20.00%

of Y

|

16,000.00

|

|

Malaysia

Small & Mid Cap

|

8.00%

of Y

|

6,400.00

|

|

Gold

& Precious Metals

|

10.00%

of Y

|

8,000.00

|

|

Global

REITS

|

7.50%

of Y

|

6,000.00

|

|

TOTAL

|

100,000.00

|

Review

Once you've completed your portfolio of investment, make sure to review the performance of your portfolio every 6 months or on a yearly basis. Carry out portfolio balancing whereby profits from funds are redeemed and used to invest into funds that are making losses. This would help you to stay true to the philosophy of buying low, selling high.

Summary

In this post, I've shared my own version of creating a portfolio of unit trust funds. An investor can decide if the portfolio suits his or her risk appetite by making changes to:

1. The category of unit trust to be used in the portfolio

2. The percentage allocation of each category in the portfolio

I would also like reiterate that the creation of portfolio investment is suited for investors with lump sum to invest in. Having a portfolio of diversified investments helps lump sum investors to mitigate risk of losing all of this investment.

If your objective is to save up for retirement on a gradual basis, do take a look at the my post on Dollar Cost Averaging instead. And once you've build up a sizable amount from your consistent monthly contribution, you can then start creating your portfolio of unit trust investments too!

Cheers and Happy Investing!

P/s : Like to find out what are the specific top performing funds I suggest for each category? Then drop me an email at shanesee03@gmail.com

If you like reading this post, don't forget to

1. Share it on Facebook!

2. LIKE my Facebook Page

1. Share it on Facebook!

2. LIKE my Facebook Page

No comments:

Post a Comment