Once GST is implemented in 2015, many are expecting the inflation rate for Malaysia to increase. With that in mind, many Malaysians are searching for passive investment that could generate returns that are equal or higher then the inflation rate in order preserve the value of their savings.

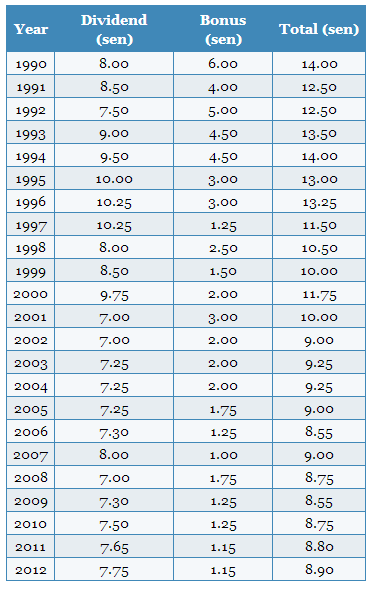

One of the popular "near" guaranteed passive investment available in Malaysia is Amanah Saham Bumiputera. Amanah Saham Bumiputera or ASB in short is one of the most seek after passive investment by Malaysian Bumiputera due to its consistent dividend and bonus. See historical dividend and bonus for ASB below:

Due to ASB's popularity, most financial/investing/personal finance blog including this one would have written extensively about ASB. In some of my older articles about ASB, I wrote with the perception that dividend and bonus from ASB can be summed into a single value in order to calculate the annual return.

|

| Historical Dividend courtesy of 1-Million-Dollar-Blog |

A BIG MISTAKE Indeed!

(Rest assured I've made the necessary amendments to my older articles)

Now if we look at dividend and bonus from a logical point of view, the fact that ASB declares dividend and bonus separately should have raised some doubts. If both are the same, why not just declare everything as dividend only!

This severe lack of understanding on the difference between dividend and bonus has lead many ASB investors to have the following misperceptions:

- Annual return is calculated based on the summation of dividend + bonus

- Dividend and bonus are calculated based on the balance in ASB account as of 31st Dec for each year

If the above are incorrect, then how exactly does ASB calculate their dividend and bonus for investors? Let's take a look...

Understanding & Calculating ASB Dividend and Bonus

ASB DividendKey Points About ASB Dividend:

- ASB Dividend and ASB Bonus are calculated differently and separately from one another.

- Dividend is calculated on a monthly basis over the duration of the year dividend is declared. We term the monthly dividend calculation as Monthly Dividend Amount.

- Total Dividend Paid for the year is the Sum of calculated Monthly Dividend Amount from Jan till Dec.

- To calculate the Monthly Dividend Amount for each month, the Lowest Account Balance for each month is used.

- Lowest Account Balance for a month is defined as the lowest value of your ASB account for that particular month. Let's see Example 1 to 3 below:

- On 1st Jan 2013, your account balance in ASB is RM5000

- You withdraw RM1000 on the 3rd of Jan 2013

- You then Redeposit RM2000 into your ASB on the 10th of Jan 2013.

- What is your Lowest Account Balance for Jan 2013?

- Answer is RM4000.00

Lowest Account Balance (Example 2):

- On 1st Jan 2013, your account balance in ASB is RM5000

- You deposit RM1000 on the 3rd of Jan 2013

- You then withdraw RM2000 from your ASB on the 10th of Jan 2013.

- What is your Lowest Account Balance for Jan 2013?

- Answer is RM4000.00

Lowest Account Balance (Example 3):

- On 1st Jan 2013, your account balance in ASB is RM5000

- You deposit RM1000 on the 3rd of Jan 2013

- You then withdraw RM500 from your ASB on the 10th of Jan 2013.

- What is your Lowest Account Balance for Jan 2013?

- Answer is RM5000.00

Formula for ASB Dividend Calculation:

Monthly Dividend Amount calculation:

Total Dividend Paid is then calculated using this formula:

ASB Bonus

Key Points About ASB Bonus

- Bonus is also calculated on a monthly basis which we term it as Monthly Bonus Amount.

- The significant difference between Bonus and Dividend is that Total Bonus Paid by ASB is the Sum of Monthly Bonus Amount calculated from the number of months you've stayed invested in ASB. However this is subjected to a maximum of 120 months or 10 years from bonus declaration year.

- In other words, ASB Bonus is calculated based on all the months over a period of 10 years starting from the year bonus is declared.

- To calculate the Monthly Bonus Amount for each month, ASB also uses the Lowest Account Balance as part of the calculation.

- Let's take a look at examples below:

No. of Months eligible for Total Bonus Calculation (Sample 1)

- You have invested into ASB since 1st Jan 2010

- ASB Bonus of 2% is declared for 2013

- How many months will be taken into consideration for Monthly Bonus Amount calculation?

- Answer : 48 months (Jan 2010 till Dec 2013)

No. of Months eligible for Total Bonus Calculation (Sample 2)

- You have invested into ASB since 1 Jan 1990

- ASB Bonus of 2% is declared for 2013

- How many months will be taken into consideration for Monthly Bonus Amount calculation?

- Answer : 120 months (Jan 2004 till Dec 2013)*

Formula for ASB Bonus Calculation:

Monthly Bonus Amount calculation:

By obtaining the Monthly Bonus Amount over a period of 120 months from the year bonus is declared,

Total Bonus Paid is then calculated using this formula:

Sample Calculations

Case Study 1 :

Invest Lump Sum of RM50,000 starting Jan 2012

ASB declared the following for 2012:

Dividend 2012 = 7.75%

Bonus 2012 = 1.15%

What is the Total Dividend Paid, Total Bonus Paid and Actual Annual Rate of Return for 2012?

Calculation:

Observation:

As you can see, the Lowest Account Balance for Jan 2012 is RM0.00 because this investment started in Jan 2012. If you've started in Dec 2011, then the Lowest Account Balance for Jan 2012 should be RM50,000.

Despite Dividend declared is 7.75% and Bonus at 1.15%, which many tend to sum up as 8.90%, we see that the Actual ASB Annual Rate of Return for 2012 is only 7.21%.

Invest Lump Sum of RM50,000 starting Jan 2011

ASB declared the following for 2011:

Dividend 2011 = 7.65%

Bonus 2011 = 1.15%

ASB declared the following for 2012:

Dividend 2012 = 7.75%

Bonus 2012 = 1.15%

What is the Total Dividend Paid, Total Bonus Paid and Actual Annual Rate of Return for 2011?

What is the Total Dividend Paid, Total Bonus Paid and Actual Annual Rate of Return for 2012?

Calculation for 2011:

Calculation for 2012:

Case Study 3 :

Invest RM500 monthly starting Jan 2012

ASB declared the following for 2012:

Dividend 2012 = 7.75%

Bonus 2012 = 1.15%

What is the Total Dividend Paid, Total Bonus Paid and Actual Annual Rate of Return for 2012?

Calculation:

Summary

Finding out how ASB calculates Dividend and Bonus has been a real eye opener for me. This changes my perception on ASB and hopefully assist others to make better decisions when it comes to investing into ASB. A clear cut example for ASB investors is maximized the Dividend and Bonus for ASB through Lump Sum investing instead of monthly. In addition, knowing how the calculation works helps you to chart your financial goals more accurately.

With that I bid all of you Cheers and Happy Investing!

If you like reading this post, it would do me a great favor by:

1. Sharing this post on your Facebook!

2. Liking my Facebook Page

You can also contact me at shanesee03@gmail.com on how to start your own long term passive investment.

2. Liking my Facebook Page

You can also contact me at shanesee03@gmail.com on how to start your own long term passive investment.