I've received quite a number of queries from friends whom already or intend to invest in an insurance saving plan as part of their investment diversification. Under most cases, my explanation to them were rather general without real figures to backup the point that it "might not" be a good option to diversify via an insurance saving plan especially if you are looking for higher returns.

In this article, I would like to illustrate the actual returns of an insurance saving plan and provide the pros and cons of investing in one.

Background

Most insurance savings plan requires an potential investor to do the following:

1. Contribute an annual premium/contribution/savings over a certain period of time. (Normally 10 years).

2. During the period of contribution, you are also protected normally for "Death & TPD". Some insurance companies do throw in additional coverage to make a plan more attractive.

3. Once you've completed paying 10 years worth of contribution you then enjoy the following benefits for the next 10, 15 or 20 years depending on the plan you choose. The benefits that one can enjoy are:

4. Obviously there's also insurance coverage during this period of the plan until it reaches maturity.

5. Once the plan reaches maturity, you will receive a lump sum cash payment including additional bonuses (determined by the insurance company)

However, I will to not further discuss the details of the insurance coverage provided by the saving plan as I believe most investors go for the insurance savings plan mainly for the cash payout and the lump sum cash returned upon maturity.

Case study of a sample insurance plan

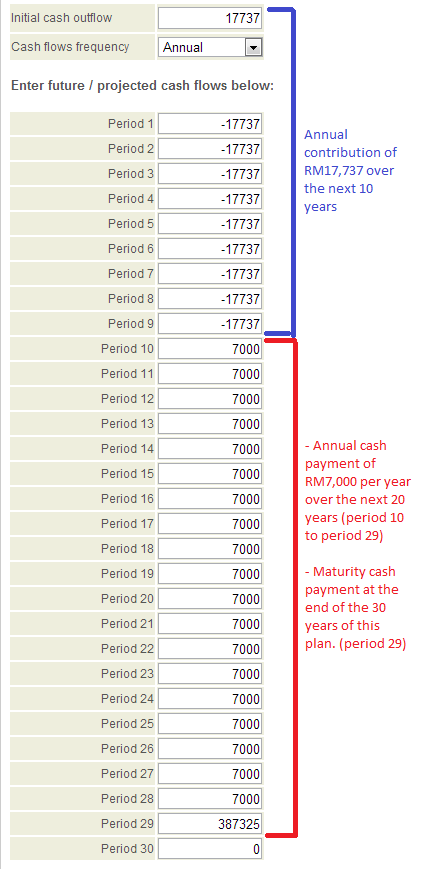

For the purpose of case study, shown below is a snapshot of an actual insurance plan:

As describe above, the client is a non-smoking male, aged 35. He has chosen a 30 years insurance saving plan that also provides insurance coverage for Death and TPD worth RM100,000.

Policy Period (first 10 years)

He has to contribute RM17,737 per annum for the next 10 years.

Next 20 years upon completion of policy payment

He will enjoy the following for the next 20 years:

1. Guaranteed cash payout of RM4,000 per annum

2. Non-guaranteed Simple Reversionary Bonus of RM3,000 per annum

When plan matures on the 30th year

He will receive a lump sum projected value of RM380,325.

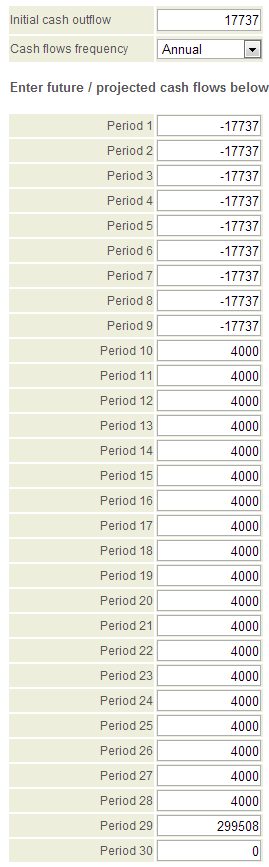

The diagram below further illustrates how the insurance saving plan works:

How much does the client stand to gain over the entire plan?

In the above snapshot (refer to the blue box), this client can "potentially" gain RM520,325. The value of RM520,325 is derived by summing up the following:

a) Guaranteed RM4,000 per annum x 20 years = RM80,000

b) Non-guaranteed annual bonus of RM3,000 x 20 years = RM60,000

c) Projected maturity value = RM380,325

Total : RM80,000 + RM60,000 + RM380,325 = RM520,325

Does that sound like a great passive investment option especially if you are only paying a total of RM177,370 in total for the first 10 years in return for RM520,325 plus insurance coverage?

Before you go about deciding to take up this insurance saving plan, let's take a deeper look into the plan and see what we can find out!

What's Guaranteed and What's Not?

In this plan, there are certain figures which are guaranteed and some figures which are only projected values.

Guaranteed annual cash payment over next 20 years:

Guaranteed RM4,000 per annum x 20 years = RM80,000

Guaranteed amount upon maturity:

Firstly, the projected maturity value of RM380,325 consist of the following components:

a) Sum assured = RM100,000 (guaranteed)

b) Terminal bonus = RM195,508 (guaranteed)

c) Simple Revisionary bonus = RM84,817 (non-guaranteed)

Guaranteed amount upon maturity : RM100,000 + RM195,508 = RM295,508

Total guaranteed value:

Consist of the sum of annual cash payment and guaranteed maturity amount:

= RM 80,000 + RM 295,508

= RM 375,508

Total non-guaranteed value:

= RM 520,325 - RM375,508

= RM 144,817

Despite knowing the guaranteed amount and the projected amount, we are still unclear if investing in this insurance saving plan is worthwhile or not? An investment worthiness is normally determined through its annul returns in %. Knowing the actual annual returns of an investment is vital especially if you are deciding if the investment returns ensuring that your money is growing faster then the depreciation rate (in other words, inflation).

What is the Actual Annual Returns (%) for this Insurance Saving Plan?

Considering that

this saving plan is not a straightforward investment that require you to invest a large amount at one go and then enjoy fixed % return yearly over the next 30 years, we will need to calculate the annual returns using what we call an

Internal Rate of Return (IRR) calculation.

IRR Calculation (Inclusive of Guaranteed and Non Guaranteed Amount)

In order to perform the IRR calculation, I am using an online IRR calculator from

vindeep.com

Summary of IRR Calculation

Based on the IRR calculation, if this insurance saving plan is able to generate a projected total return of RM520,325 at the end of 30 years based on your total contribution of RM177,370 for the first 10 years, the annual percentage return is 5.17% per annum

If the IRR calculation is done entirely on the guaranteed value of RM375,508 only, the annual percentage return of this insurance saving plan is a meager 3.44% per annum.

Summary

Based on the IRR calculation, you can see that the guaranteed value provided by this insurance saving plan is about 3.44% per annum. This figure is slightly higher then the Fixed Deposit rate offered by the bank.

As for the projected total return of 5.17% per annum, do remember that this is just a projected figure that might or might not be achievable. We can only be assured of the 3.44% returns per annum as guaranteed by this plan.

Investment returns aside, investing into an insurance saving plan provides you with a form of protection in the event of a Death or TPD. Further more, since there is an element of insurance from subscribing to this plan, you can use it for tax rebate purpose.

Cheers and Happy Investing!

P.s : The calculation of IRR is up for debate. If you feel that I've made a mistake in calculating the IRR or misinterpreted this insurance saving plan, feel free to post a comment here.

If you like reading this post, it would do me a great favor by:

1. Sharing this post on your Facebook!

2. Liking my Facebook Page

You can also contact me at shanesee03@gmail.com for further questions/inquiries.