A Merry Christmas and A Happy New 2014 Year from Invest Made Easy

We hope all your financial goals will be achieved and all investments turn fruitful!

|

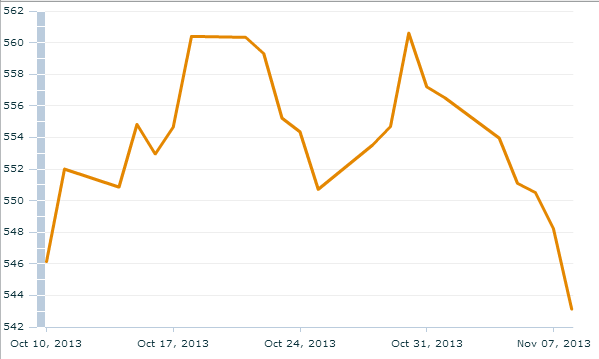

| IRR = 3.62% |

|

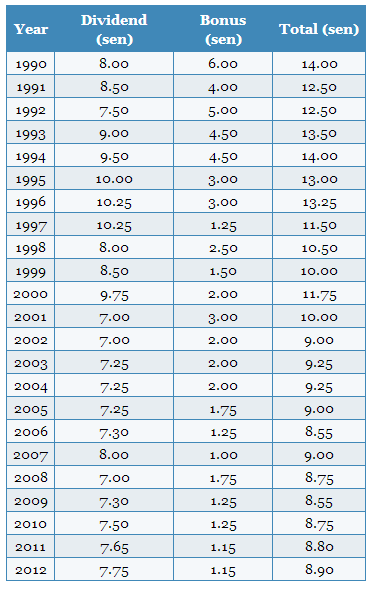

| Historical Dividend courtesy of 1-Million-Dollar-Blog |

|

| OCBC MaxEdu Choice - Click to Enlarge |

|

| Click to Enlarge |

|

| Top 10 Best Performing Unit Trust Fund (Equity Malaysia) |

Fund Name

|

YTD as of

9th Oct 2013 |

YTD as of

8th Nov 2013 |

4 Weeks

Gain / Loss (%) |

4 Weeks Gain/

Loss Rankings |

Previous

4 Weeks Gain/Loss Rankings |

Phillip Master Equity

Growth Fund

|

27.64

|

32.1

|

4.46

|

1

|

1

|

Kenanga Growth Fund

|

16.21

|

18.98

|

2.77

|

3

|

7

|

CIMB-Principal Wholesale

Equity Fund

|

16.05

|

20.5

|

4.45

|

2

|

5

|

MAAKL-HDBS Flexi Fund

|

13.27

|

15.13

|

1.86

|

5

|

4

|

CIMB-Principal Equity

Fund

|

16.25

|

18.52

|

2.27

|

4

|

2

|

Kenanga Syariah Growth

Fund

|

15.99

|

17.7

|

1.71

|

6

|

6

|

Hwang AIIMAN Growth

|

17.63

|

20.4

|

2.77

|

3

|

3

|

Public Focus Select Fund

|

Newcomer

|

7.91

|

N/A

|

N/A

|

N/A

|

Public Islamic

Opportunities Fund

|

Newcomer

|

24.58

|

N/A

|

N/A

|

N/A

|

Public Regular Savings

Fund

|

Newcomer

|

12.78

|

N/A

|

N/A

|

N/A

|

AVERAGE 4 WEEKS GAIN/LOSS (%)

|

2.90

|

||||

Fund Name

|

YTD as of

9th Oct 2013 |

YTD as of

8th Nov 2013 |

4 Weeks

Gain / Loss (%) |

4 Weeks Gain/

Loss Rankings |

Previous

4 Weeks Gain/Loss Rankings |

Public Islamic Asia

Dividend Fund

|

3.15

|

3.76

|

0.61

|

3

|

3

|

Pheim Asia Ex-Japan

Islamic

|

13.47

|

14.35

|

0.88

|

2

|

1

|

Public Asia Ittikal Fund

|

1.88

|

2.12

|

0.24

|

7

|

5

|

Public Regional Sector

Fund

|

15.26

|

15.36

|

0.1

|

9

|

7

|

PB Islamic Asia Equity

Fund

|

1.46

|

1.91

|

0.45

|

5

|

4

|

Eastspring Investments

Asia Pacific Shariah Equity Fund

|

-0.25

|

-0.07

|

0.18

|

8

|

6

|

Pheim Asia Ex-Japan

|

2.67

|

3.22

|

0.55

|

4

|

N/A

|

CIMB Islamic Asia Pacific

Equity Fund

|

3.15

|

4.56

|

1.41

|

1

|

8

|

MAAKL Pacific Fund

|

4.21

|

4.59

|

0.38

|

6

|

2

|

Public Far-East Select

Fund

|

9.36

|

8.67

|

-0.69

|

10

|

N/A

|

AVERAGE 4 WEEKS GAIN/LOSS (%)

|

0.41

|

||||

|

Fund Name

|

YTD as of

9th Oct 2013 |

YTD as of

8th Nov 2013 |

4 Weeks

Gain / Loss (%) |

4 Weeks Gain/

Loss Rankings |

Previous

4 Weeks Gain/Loss Rankings |

|

CIMB-Principal Greater

China Equity Fund

|

7.73

|

7.02

|

-0.71

|

4

|

2

|

|

PB China Pacific Equity

Fund

|

9.3

|

8.26

|

-1.04

|

7

|

6

|

|

Public China Ittikal Fund

|

6.57

|

6.18

|

-0.39

|

1

|

5

|

|

Public China Select Fund

|

10.08

|

9.12

|

-0.96

|

5

|

4

|

|

PB China Titans Fund

|

4.53

|

3.88

|

-0.65

|

3

|

8

|

|

MAAKL Greater China Fund

|

2.54

|

1.55

|

-0.99

|

6

|

7

|

|

AmIslamic Greater China

|

-2.67

|

-3.31

|

-0.64

|

2

|

3

|

|

Eastspring Investments

Dinasti Equity Fund

|

5.69

|

3.8

|

-1.89

|

8

|

9

|

|

Hwang China Select Fund

|

17.91

|

15.43

|

-2.48

|

9

|

1

|

|

Manulife Investment -

China Value Fund

|

Newcomer

|

7.61

|

N/A

|

N/A

|

N/A

|

|

AVERAGE 4 WEEKS GAIN/LOSS (%)

|

-1.08

|

||||